Anything less than 3% is extremely optimistic even for us marketAll a guessing game but I do think we will follow closely with the US, this is their prediction

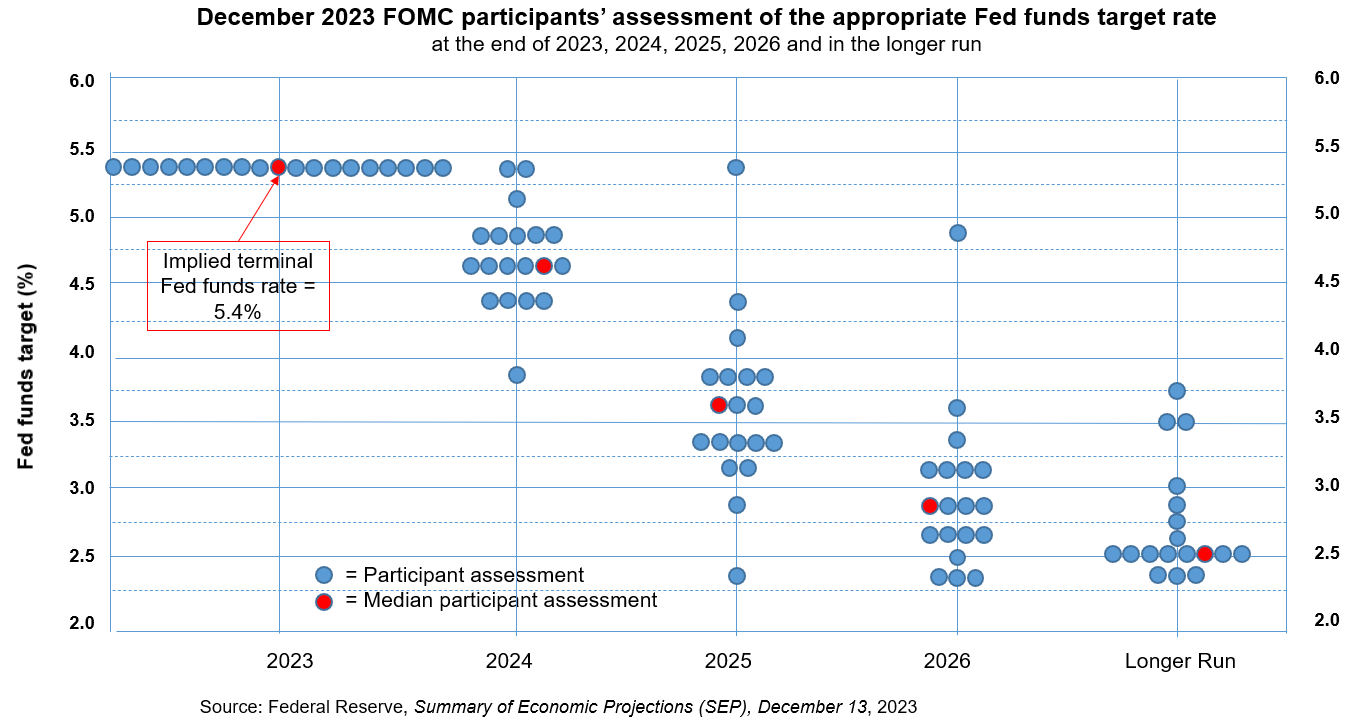

2024 - 4.6%

2025 - 3.6%

2026 - 2.9%

Fed signals end of rate hikes and projects cuts in 2024

The Federal Reserve signaled at its meeting on Wednesday that it is done raising its policy rate and is poised to reduce it by 75 basis points next year, with more cuts after that.realeconomy.rsmus.com

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Mortgage Rate Rises

- Thread starter glenimp617

- Start date

More options

Thread starter's posts3 years left on my current deal @1.19%.

25 years left on the mortgage but if all goes well should be done in 5.

yep we took 5 years as it means our final amount is low - it did mean we paid for a chunk between the two mortgages. We can pay off in 3 but we don’t know the job market situation hence going 5.

Last edited:

Anything less than 3% is extremely optimistic even for us market

I'd say it's optimistic but not extremely.

Inflation is nearly under 2pc there. If it stays there no reason it can't come down fairly sharp.

I'd say it's optimistic but not extremely.

Inflation is nearly under 2pc there. If it stays there no reason it can't come down fairly sharp.

I think that 3%+ rates are here to stay for at least the next 4 years. They want to tar as many people as possible, the people who renewled their mortage just before the rates went up would have lucked out if the rates are dropped before then.

lower than 3% is not a common thing, it was only dropped that low to make up for the housing crash in 2008 and they never took them back up.

I'm hoping for a rate around 3.2% when I have to remortage in 4 years time and I'm going to attempt to pay it all off in 5 years.

Well I hope it's not 3.3%, you'd be screwed then...I think that 3%+ rates are here to stay for at least the next 4 years. They want to tar as many people as possible, the people who renewled their mortage just before the rates went up would have lucked out if the rates are dropped before then.

lower than 3% is not a common thing, it was only dropped that low to make up for the housing crash in 2008 and they never took them back up.

I'm hoping for a rate around 3.2% when I have to remortage in 4 years time and I'm going to attempt to pay it all off in 5 years.

I know it's not a particularly relevant benchmark given what it preceded but there's no law stating mortgages are base rate PLUS..

In the 00s it was totally normally for them to be advertised as base rate MINUS.

I can see us getting back to something a bit like that as they start coming down, nothing like the 00s but entirely possible as competition hots up.

In the 00s it was totally normally for them to be advertised as base rate MINUS.

I can see us getting back to something a bit like that as they start coming down, nothing like the 00s but entirely possible as competition hots up.

not really as it's still less that my rate that the moment.Well I hope it's not 3.3%, you'd be screwed then...

Anybodies guess to where the rate will settle but just remember 0% period should not be considered the historic norm so I wouldn't be expecting old interest rates to resurface. After briefly being on variables at 8% and now 7% I'm primed to be happy with a low 4 or delighted with a mid 3 % rate

Soldato

- Joined

- 4 Aug 2007

- Posts

- 22,433

- Location

- Wilds of suffolk

I know it's not a particularly relevant benchmark given what it preceded but there's no law stating mortgages are base rate PLUS..

In the 00s it was totally normally for them to be advertised as base rate MINUS.

I can see us getting back to something a bit like that as they start coming down, nothing like the 00s but entirely possible as competition hots up.

Thats not really true unfortunately.

The only real product that was "base rate -" were trackers.

The majority were moving back to repayment at that point, but there were still some endowment backed and interest only was becoming the next best thing. None of these were "base rate -" products.

Most big businesses were linking LIBOR and this gave the impression interest rates were often below base rate, but they were simply unlinked.

Edit, and the point of the base rate is its supposed to set the minimum level, outside specials. If everyone started to ignore the base rate then you would expect some action from the regulators and/or government. Its there for a reason!

Last edited:

I knew NZ was an expensive place to live (in certain areas at least), but I didn't realise Australia was suffering from crazy house prices too:

https://www.bbc.co.uk/news/business-66425947

Which 'nice' countries have sensibly priced housing these days?

https://www.bbc.co.uk/news/business-66425947

Which 'nice' countries have sensibly priced housing these days?

There is plenty of cheaper (or even just cheap) housing in Australia outside of the big cities but outside of the big cities is not where people want to live.

But to answer your a question, America is the other option but again you’ll not be near any big cities, you’ll be out in the boonies.

But to answer your a question, America is the other option but again you’ll not be near any big cities, you’ll be out in the boonies.

I knew NZ was an expensive place to live (in certain areas at least), but I didn't realise Australia was suffering from crazy house prices too:

https://www.bbc.co.uk/news/business-66425947

Which 'nice' countries have sensibly priced housing these days?

The issue is the same all over - people want/need to live in the city in order to get to work, however there is not enough housing being built to satisfy the demand to keep prices low.

It's the exact same issue that's impacting London

UK Interest Rate History / Graph

Historical UK Interest Rates data since 1975, including graphs and data to show historical trends, and how they compare with recent rates.

www.propertyinvestmentproject.co.uk

www.propertyinvestmentproject.co.uk

As per historic rates in the uk... this page since 1975... sub 3% rates is not the norm only been a thing since the housing market crash of 2008.

Associate

- Joined

- 21 Aug 2010

- Posts

- 754

This is exactly the data that made me comfortable with locking in to long fixed rates.UK Interest Rate History / Graph

Historical UK Interest Rates data since 1975, including graphs and data to show historical trends, and how they compare with recent rates.

As per historic rates in the uk... this page since 1975... sub 3% rates is not the norm only been a thing since the housing market crash of 2008.

This is exactly the data that made me comfortable with locking in to long fixed rates.

I bought in '82 and finished in 2009. Mostly it was variable too, fixes were not a thing at that time.

You are correct - the UK rates should be in the 4%-6% range when our economy is healthy.UK Interest Rate History / Graph

Historical UK Interest Rates data since 1975, including graphs and data to show historical trends, and how they compare with recent rates.

As per historic rates in the uk... this page since 1975... sub 3% rates is not the norm only been a thing since the housing market crash of 2008.

The current problem isn't the rate, it's the speed of the fact that we went from 10 years of near zero rates, to over 5% without the rest of the economy (eg. wages) having time to adjust.

People will slowly adjust to the higher rates and not over reach when it comes to buying houses, this should slow down the appreciation rate of house prices.You are correct - the UK rates should be in the 4%-6% range when our economy is healthy.

The current problem isn't the rate, it's the speed of the fact that we went from 10 years of near zero rates, to over 5% without the rest of the economy (eg. wages) having time to adjust.

Mine has dropped over in the last year, when it was last appraised for a mortage renewl, not by much but it's likely been adjusted due to the higher mortage rates.