You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Best savings account?

- Thread starter Merlin5

- Start date

More options

Thread starter's poststrading 212 is still the "best" in terms of flexibility and rates I think

Although the rates are getting silly low

Id have a look at Stocks ISA But may just stick to Cash ISA..

Evening all, What Cash ISA's would you all recommend using? I've got one on my Lloyds app but ideally I'd like one separate?

Check the ISA section on money saving expert... They update thier list of top ISAs regularly.

Rates aren't great across the board at the moment though as the BOE has been reducing the base rate steadily for some time now, so they are all tracking that to some extent.

Also watch out for accounts offering high 'bonus rates for X months' as after the honeymoon period they often drop down to a lower variable rate than the competition...

So as always.. Do the maths to see if it's as good as it looks on the surface.

New savings account, may be of interest to someone. DYOR etc...

'Digital bank Zopa has entered the current account market, offering customers 2% interest on balances, cashback and 7.10% interest on a linked savings account.

Here are the key details:

'Digital bank Zopa has entered the current account market, offering customers 2% interest on balances, cashback and 7.10% interest on a linked savings account.

Here are the key details:

- The Biscuit current account offers 2.00% AER

- A linked regular saver account offers 7.10% interest on deposits of up to £300 a month for one year

- The saver account becomes a 3.5% easy access savings account after a year, but customers can then open another regular saver

- There's also 2.00% cashback on bills on up to £1,500 of direct debits per year'

trading 212 is still the "best" in terms of flexibility and rates I think

Although the rates are getting silly low

You say that, but my rate with trading 212 is dropping this month i believe to 4.1% is it ?

My bonus rate ends in a couple of days

Last edited:

Soldato

- Joined

- 23 May 2006

- Posts

- 8,482

i have just had my 1st ever punt on an investment isa. i know nothing about them but i figure its only a small percentage of my savings (this years full ISA allotment). its an FTSE All - world ISA with Chip / HSBC medium:High risk.

its waaay out of my comfort zone as i am mr play it safe with cash isas etc but its somthing interesting to follow i guess and am prepared to stick the money in and leave it in for the long term.

its waaay out of my comfort zone as i am mr play it safe with cash isas etc but its somthing interesting to follow i guess and am prepared to stick the money in and leave it in for the long term.

Last edited:

That's still the highest non boosted cash ISA rate I think (flexible)You say that, but my rate with trading 212 is dropping this month i believe to 4.1% is it ?

My bonus rate ends in a couple of days

It's just that overall the rate is crap now.

Personally I'm keeping 10k in a cash ISA, basically emergency funds.

Then dumping the rest into sp500 (after pension maxed out)

Last edited:

That's still the highest non boosted cash ISA rate I think (flexible)

I've got some money in a 90 day notice account (oxbury) thats paying 4.5% currently, thats not in an isa though...my ISA is already full for this year...

i have just had my 1st ever punt on an investment isa. i know nothing about them but i figure its only a small percentage of my savings (this years full ISA allotment). its an FTSE All - world ISA with Chip / HSBC medium:High risk.

its waaay out of my comfort zone as i am mr play it safe with cash isas etc but its somthing interesting to follow i guess and am prepared to stick the money in and leave it in for the long term.

You'll be fine.. I put my full 20k into stocks and shares ISA this year.. and the returns are ******* all over my cash ISA which has 40k in it...

Don't check it day to day, you'll have a heart attack... just buy into a sensible ETF such as VWRP, and maybe a smaller second ETF such as VEUA)

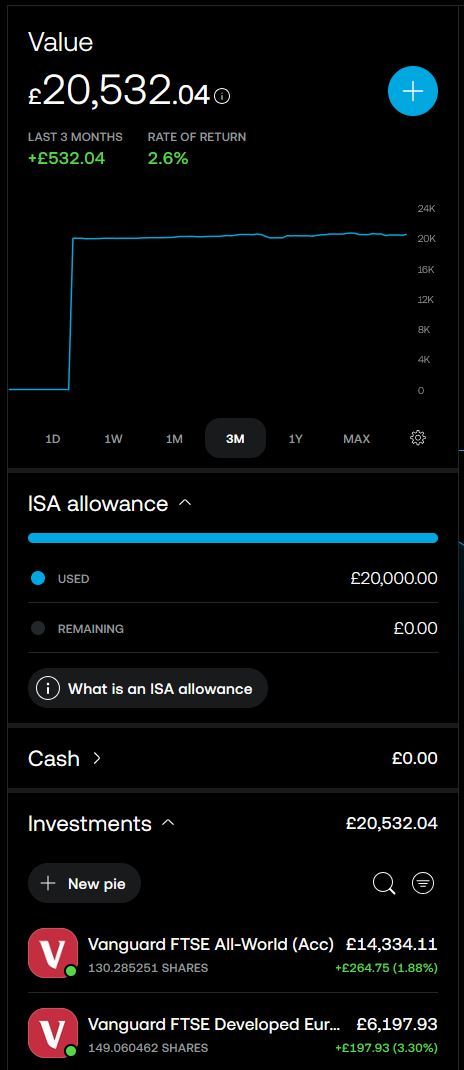

This is what I did in april, and I'm about £500 up in 3 months...

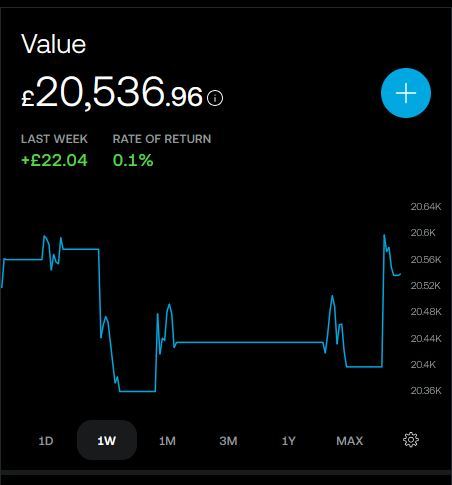

That looks great, but if I look at last weeks performance, it looks like a heart attack...

The thing with ETFs are they are long term, so try not to look at it on a daily or even weekly basis, stick with a diverse global fund, which it sounds like you have, and...wait..and wait.. and wait...

Last edited:

What about my instant gratification! (I'm doing £500 a month into the 212 stock ISA on all world acc at the moment)wait..and wait.. and wait...

Paid mortgage off then just diverted that payment into the ISA instead

Last edited:

What about my instant gratification! (I'm doing £500 a month into the 212 stock ISA on all world acc at the moment)

Paid mortgage off then just diverted that payment into the ISA instead

Risk strategy is all i'll say...

Sure you can win big by day-trading stocks, but you can also very easily lose big too!

I'm doing £500 a month into the 212 stock ISA on all world acc

'Doing' as in profit? How much is in your s&s ISA? It'll have to be a shed load more than 20k for that sort of return if it's an ETF!!

Last edited:

Soldato

- Joined

- 14 Jul 2005

- Posts

- 9,388

- Location

- Birmingham

New savings account, may be of interest to someone. DYOR etc...

'Digital bank Zopa has entered the current account market, offering customers 2% interest on balances, cashback and 7.10% interest on a linked savings account.

Here are the key details:

- The Biscuit current account offers 2.00% AER

- A linked regular saver account offers 7.10% interest on deposits of up to £300 a month for one year

- The saver account becomes a 3.5% easy access savings account after a year, but customers can then open another regular saver

- There's also 2.00% cashback on bills on up to £1,500 of direct debits per year'

Trying to find the details of 2% cash back. It seems it's applicable to all direct debits, purpose indifferent. If it includes my mortgage then that's quite a large number as I'll be approaching the £1500 a month cap which is £30 a month just in cash back.

Soldato

- Joined

- 23 May 2006

- Posts

- 8,482

i tried that with trading some BTC and buying a crypto.com debit card (with admittedly some nice perks - since massively scaled back!!!) lets just say i am done with instant gratification as well as any delusions of becoming a crypto king!!!.What about my instant gratification! (I'm doing £500 a month into the 212 stock ISA on all world acc at the moment)

Paid mortgage off then just diverted that payment into the ISA instead

I mean paying 500 a month in haha not what it's earning! It's only got a couple grand in atm (overall in green)

Just keep pumping that monthly spare cash into it then... it's very difficult to work out the precise profit Vs a standard savings account that pays 4.x% AER for example.

If I extrapolate my S&S isa, which has only been running since April 2025, I'm running at about 8% for the year CURRENTLY, but the maths gets really fuzzy, because stocks and shares prices go up and down all the time on a daily or weekly basis, especially when there's wars and trade-wars and well, you know...

EDIT: that's why it's sensible to go for an 'all world ETF' and play the long game.

Last edited:

Soldato

- Joined

- 14 Jul 2005

- Posts

- 9,388

- Location

- Birmingham

Ah found the catch. The cap is £1500 direct debits PER YEAR not per month. So £30 per year maximum or £2.50 a month. So its rubbish. A single council tax monthly DD or energy DD will hit that cap on its own.Trying to find the details of 2% cash back. It seems it's applicable to all direct debits, purpose indifferent. If it includes my mortgage then that's quite a large number as I'll be approaching the £1500 a month cap which is £30 a month just in cash back.

Last edited:

Ah found the catch. The cap is £1500 direct debits PER YEAR not per month. So £30 per year maximum or £2.50 a month. So its rubbish. A single council tax monthly DD or energy DD will hit that cap on its own.

A lot of these 'deals' look great on the surface, but the devil is in the detail!

It really annoys me..just advertise what you actuallyoffer, don't muddy the waters by blurring the edges of the product you are offering with millions of caviats, it should be illegal, IMO...

Soldato

- Joined

- 14 Jul 2005

- Posts

- 9,388

- Location

- Birmingham

To be fair it does say per year quite prominently. I just didn't read it as that, because I don't think of my bills that way, as I suspect most people don't.A lot of these 'deals' look great on the surface, but the devil is in the detail!

It really annoys me..just advertise what you actuallyoffer, don't muddy the waters by blurring the edges of the product you are offering with millions of caviats, it should be illegal, IMO...