You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Best savings account?

- Thread starter Merlin5

- Start date

More options

Thread starter's postsCan't wait for the BoE to announce rates will be held until DJMK's mortgage is up for renewal

I'll admit to saving more and spending less than usual as the rates are high. I'd also like to buy a house one day so a lower mortgage rate would be welcome.

Lower mortgage rates = more affordable borrowing = higher house prices

It's all an intrinsically linked balancing act...

High base rate is great for saving but bad for borrowing.

Low interest is is great for borrowing but has for saving.

I don't think there can ever be a perfect balance, but just a fluctuation within sensible parameters.

If you are mortgage free then high interest is great...

If you have a mortgage but also want to save money it's more complicated as then you need do the maths as to whether you should overpay your mortgage where possible instead of saving.

High base rate is great for saving but bad for borrowing.

Low interest is is great for borrowing but has for saving.

I don't think there can ever be a perfect balance, but just a fluctuation within sensible parameters.

If you are mortgage free then high interest is great...

If you have a mortgage but also want to save money it's more complicated as then you need do the maths as to whether you should overpay your mortgage where possible instead of saving.

Base rate is there to.balance inflation in the economy. Higher rate = more restriction. Lower rate = looser financial conditions, more money creation and more growth. The mortgage issue is just a side effect of the UK having people on short term fixes, other countries with 25/30 Yr fixed rates don't see this issue.It's all an intrinsically linked balancing act...

High base rate is great for saving but bad for borrowing.

Low interest is is great for borrowing but has for saving.

I don't think there can ever be a perfect balance, but just a fluctuation within sensible parameters.

If you are mortgage free then high interest is great...

If you have a mortgage but also want to save money it's more complicated as then you need do the maths as to whether you should overpay your mortgage where possible instead of saving.

It's why I can see @danlightbulb argument more than djmk. Nobody cares if people get 1% less on their savings.

Getting 3% on savings with inflation at 2% is much better than getting 5% with inflation at 10% like it was recently.. however that point is lost on most people.

Last edited:

Base rate is there to.balance inflation in the economy. Higher rate = more restriction. Lower rate = looser financial conditions, more money creation and more growth. The mortgage issue is just a side effect of the UK having people on short term fixes, other countries with 25/30 Yr fixed rates don't see this issue.

It's why I can see @danlightbulb argument more than djmk. Nobody cares if people get 1% less on their savings.

Getting 3% on savings with inflation at 2% is much better than getting 5% with inflation at 10% like it was recently.. however that point is lost on most people.

Yeah that's kinda what I meant but made my point badly... The government/treasury and the central bank are always playing a balancing act.

Saying interest is better higher or lower is only part of the picture.

If your shopping bill is 2% higher then it's not going to be any help if your savings interest is 2% lower etc.

What's a decent instant access saver to deposit and keep ~£10k in? I have it in 212 ISA at the moment but a few times the withdrawals haven't been as fast as I'd like. I see Chase have just boosted their saver (again), but curious if there's something better.

What's a decent instant access saver to deposit and keep ~£10k in? I have it in 212 ISA at the moment but a few times the withdrawals haven't been as fast as I'd like. I see Chase have just boosted their saver (again), but curious if there's something better.

The easy answer to that is to go on the MSE website.. They update the top recommendations on a regular basis.

They don't cover every single savings product available, but they will give you a good idea of what the most competitive rates are that are currently available.

Top savings accounts

Find the top interest rate savings accounts & maximise your returns with Martin Lewis' guide. Includes the top easy-access and fixed-rate accounts to help you find the most profitable home for your cash – and keep it safe.

Last edited:

You have to look at the caviats though... Cahoot are paying 5% which is fantastic.. Until you read they don't pay interest on balances over £3k, which makes it basically useless unless you are starting out on your saving journey and don't have much money

I got sent an email today about my trading 212 cash ISA which says it's changing its terms and conditions so that they can change the rate down to 0.15% lower than the current base rate on August 4th. This will make it 4.10% which is what it currently is on anyway.

Have they done this in preparation for an additional base rate change they are predicting to happen on the next BOE meet on 7th August? i.e. 4.25% down to 4.0%, so that they can change it down to 3.85%?

Have they done this in preparation for an additional base rate change they are predicting to happen on the next BOE meet on 7th August? i.e. 4.25% down to 4.0%, so that they can change it down to 3.85%?

I got sent an email today about my trading 212 cash ISA which says it's changing its terms and conditions so that they can change the rate down to 0.15% lower than the current base rate on August 4th. This will make it 4.10% which is what it currently is on anyway.

Have they done this in preparation for an additional base rate change they are predicting to happen on the next BOE meet on 7th August? i.e. 4.25% down to 4.0%, so that they can change it down to 3.85%?

I think its because it's already priced in (I hope) as my cash ISA with them has been 4.1% for quite a while as I never had any perks on it, such as a temporarlaily higher rate for a honeymoon period, etc.

I might be totally wrong though. If it goes too low and the competition offers a better, no frills variable rate, it won't take me too much prodding me to jump ship and port my cash ISA over to A.N.Other.

From the providers perspective, they have to offer a high enough rate to compete with other ISA providers, or people will just leave.

Last edited:

Can't wait for the BoE to announce rates will be held until DJMK's mortgage is up for renewal

I'll admit to saving more and spending less than usual as the rates are high. I'd also like to buy a house one day so a lower mortgage rate would be welcome.

People spending more isn't going to help a global economy..

Stopping wars will help the global economy. And stop corrupt politicians.

I'm saving because I want to be able to live comfortably and also use the additional interest to add to.help to paying the mortgage back.

Last edited:

Simply not true. Consumer spending makes up the majority of the GDP of most major modern economies.People spending more isn't going to help a global economy..

You are already in an incredibly privileged position having a mortgage and £40k+ plus in savings. You're obviously not in the position where a percentage swing in mortgage rates is the difference between having a home and not like a lot of people.People spending more isn't going to help a global economy..

Stopping wars will help the global economy. And stop corrupt politicians.

I'm saving because I want to be able to live comfortably and also use the additional interest to add to.help to paying the mortgage back.

Low rates (especially very low rates as seen until a couple of years ago) also means more wealth transfer upwards and higher wealth inequality.Base rate is there to.balance inflation in the economy. Higher rate = more restriction. Lower rate = looser financial conditions, more money creation and more growth.

Low rates (especially very low rates as seen until a couple of years ago) also means more wealth transfer upwards and higher wealth inequality.

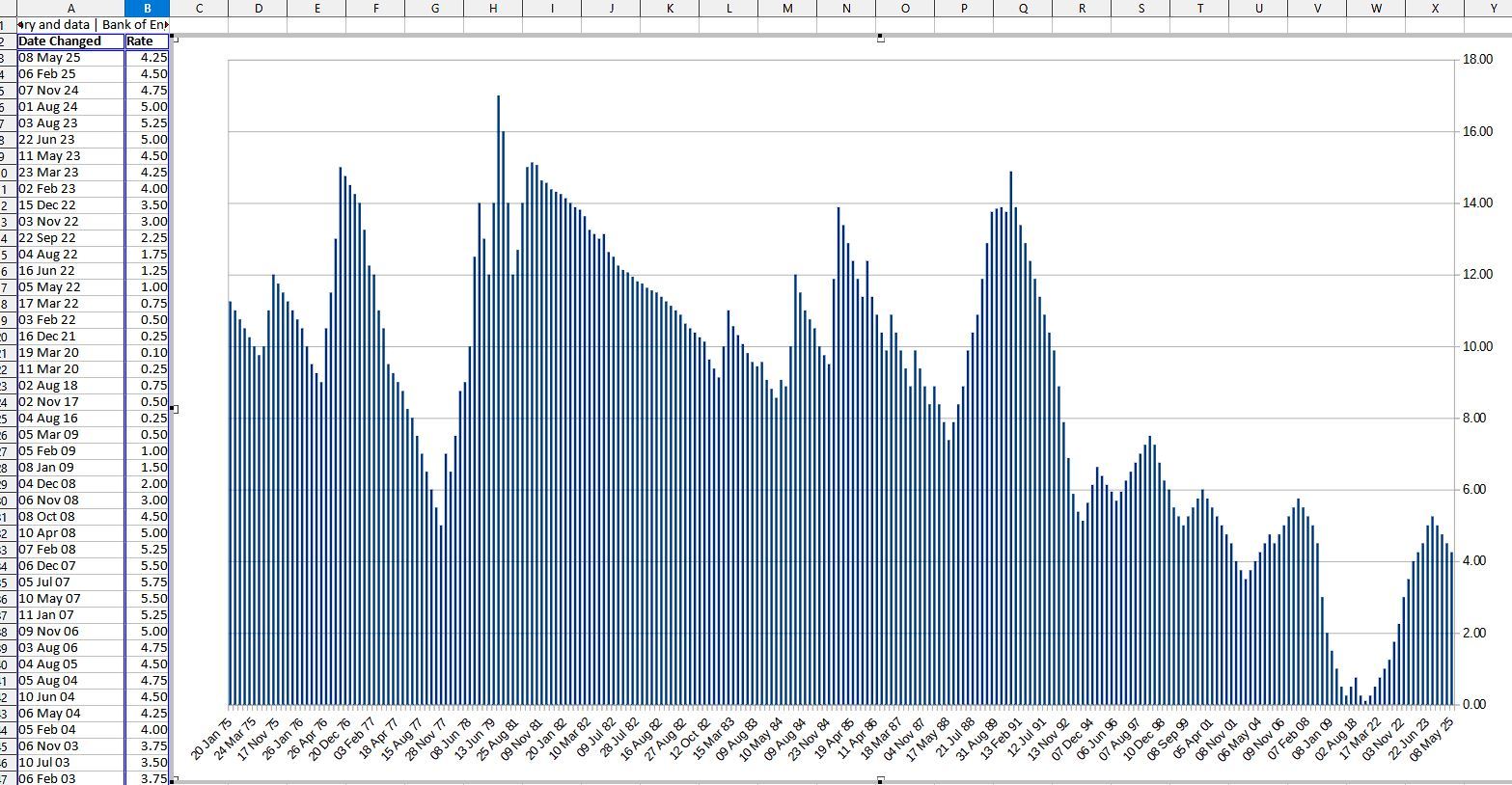

A lot of people seem to forget/deny just how unusual it was for interest rates to be that low. Without searching for exact data, I seem to recall that when looked at long term the average UK interest rate is over 7%.

A lot of people seem to forget/deny just how unusual it was for interest rates to be that low. Without searching for exact data, I seem to recall that when looked at long term the average UK interest rate is over 7%.

Out of curiosity, I just downloaded the data from the bank of england and dumped it into a graph

Last edited:

Consider also the amount of debt today to buy a house is higher so lower rates feel worse than they appear. Something all those boomers screaming about how they had 15% rates conveniently ignore.

Indeed... "we struggled with high interest"

Yeah but you bought a 4 bed detached new build with a double garage for £40k

They were pretty much pointless anyway, can do the same thing with a MMF in a s&s isa.Is it pretty much confirmed they are cutting the cash ISA amount making it pretty much pointless?