Problem with fixed rate accounts is you'll be locked in at a crap rate...

I had ~40k in my cash ISA but i moved 20k of it out and into my S&S isa last week so now my s&s ISA is bigger than my cash ISA

A couple of questions

When the BoE base rate drops .does this effect s&s ISA ?

Another question .fixed rate cash ISAs I see earn interest monthly or annually.. if you access the interest earned do you get penalised with withdrawing any interest ? Or do you only get penalised on withdrawing from the balance not the interest ?

Because I have around 80% on what you can get FCA protected on in the cash ISA

Was looking at stocks and shares but I probably.wont (move it) per say unless the rates on the.cash ISA drop hugely.

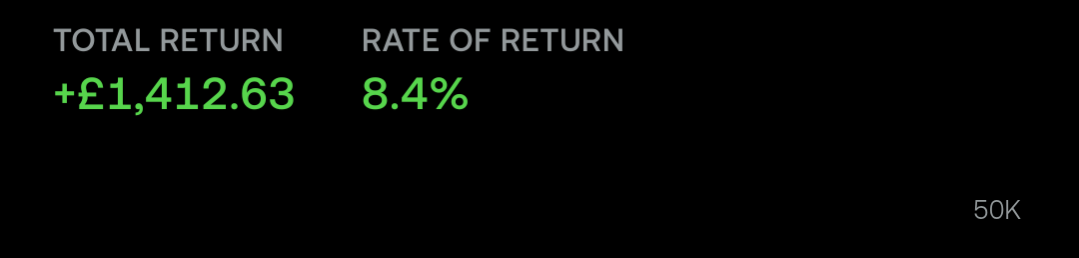

Stocks and shares again is longer term. I want compounding monthly results or earnings ideally but I do want to test s&s