Soldato

- Joined

- 4 Aug 2007

- Posts

- 22,155

- Location

- Wilds of suffolk

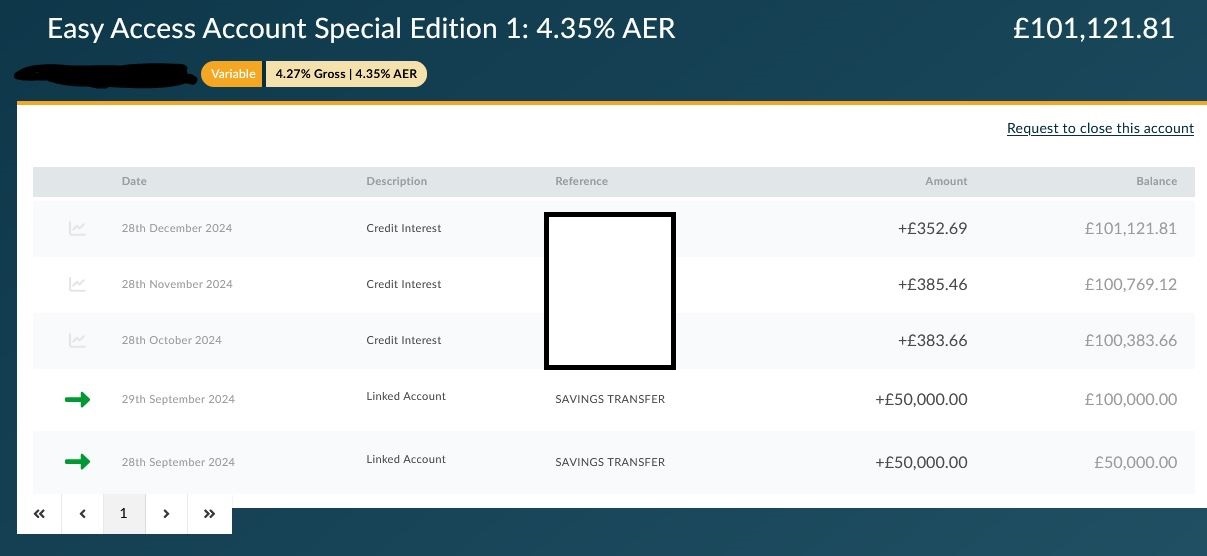

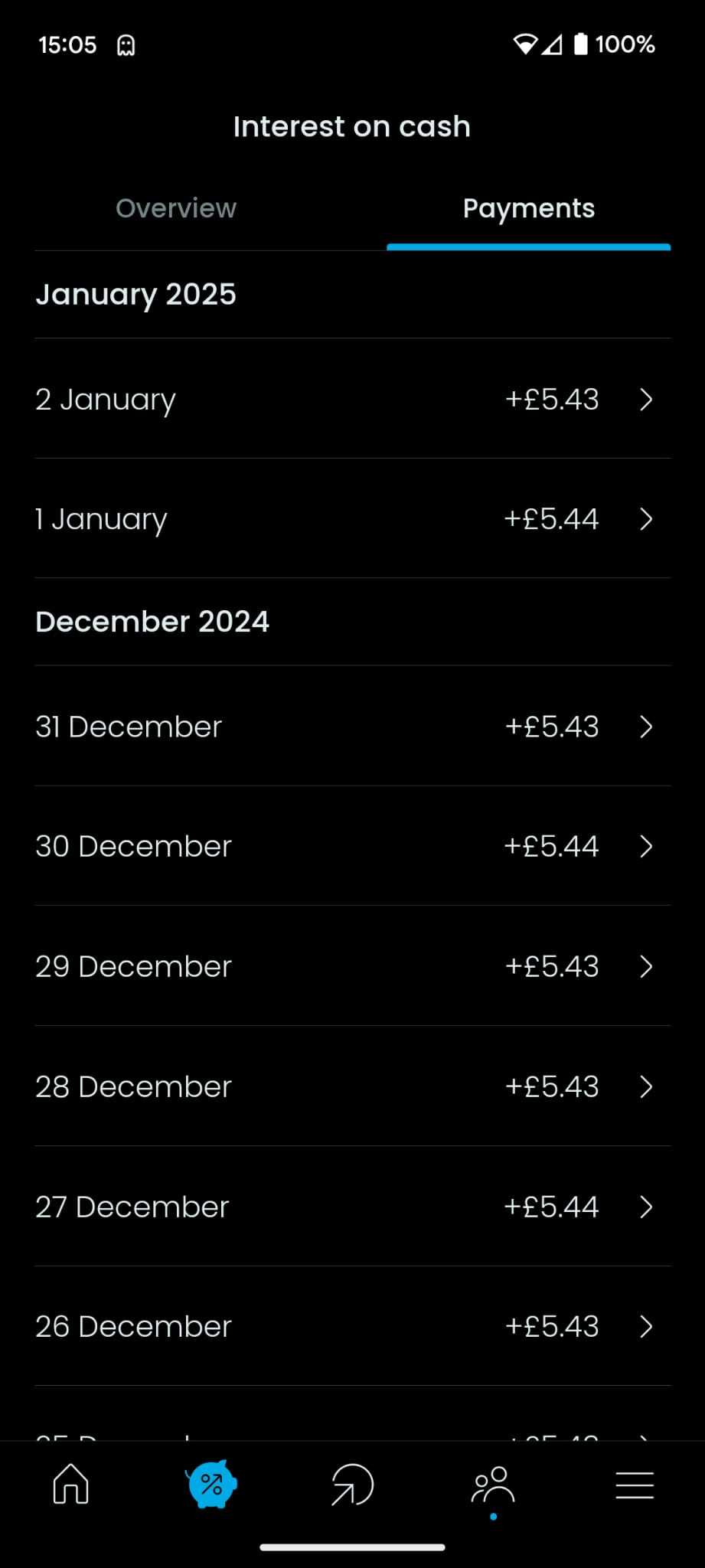

That's the weird thing - I ported the ISA over from chip, and that was the same (some months less interest than previous month) but monthly paid...and they were paying more with a lower interest rate...

I'm obvioulsy missing something...

Monthly interest normally varies by days in month.

")