You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Help to Buy Scheme Should Really Be Named Help For Bankers Scheme - Discuss

- Thread starter radderfire

- Start date

More options

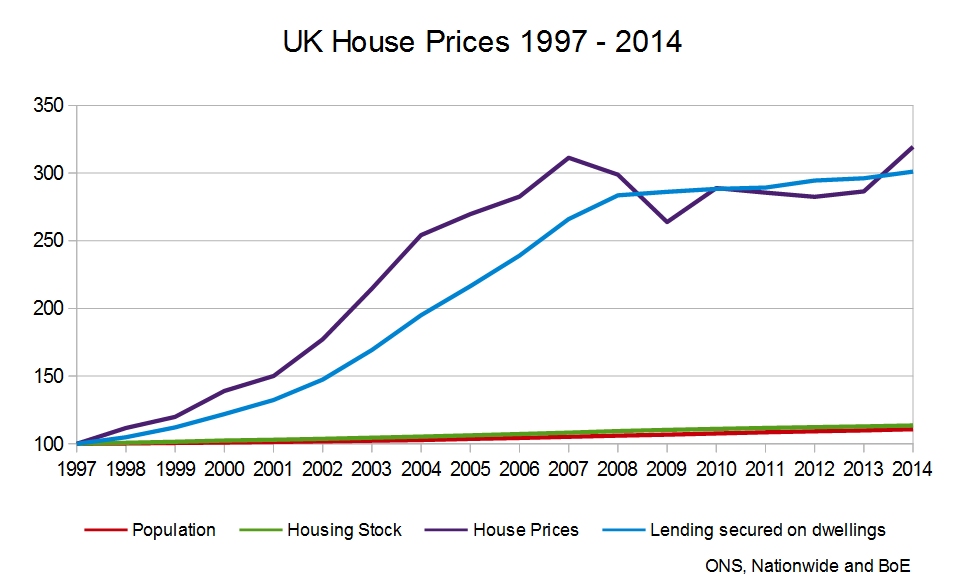

Thread starter's postsGood graph FenixTorch. Says it all, really.

")

But to be honest, besides that point I'm not here to argue banks 'win' from HTB. I'm more about arguing how everyone loses")

Er, no. If you're borrowing 'X' amount from a bank at 'Y' amount of interest, the bank wins if you borrow more. That's maths that even I can figure out! The banks always win, even the least cynical person should know thatYes, but the benifit of the artificially high prices goes to the new build developers, not the banks.

But to be honest, besides that point I'm not here to argue banks 'win' from HTB. I'm more about arguing how everyone loses

Er, no. If you're borrowing 'X' amount from a bank at 'Y' amount of interest, the bank wins if you borrow more.

Not necessarily as the money banks are lending as mortgages they are borrowing from their savers and other banks. The more they lend the bigger the risk they take and if people default on their mortgage and house prices fall (as they did post-2007 crash) then the bigger their losses.

The basic premise that availability of credit is driving up house prices is correct, but what you also have to remember is that immediately prior to that chart interest rates on mortgages were averaging around 10% I think, certainly a lot higher than today anyway.

Er, no. If you're borrowing 'X' amount from a bank at 'Y' amount of interest, the bank wins if you borrow more. That's maths that even I can figure out! The banks always win, even the least cynical person should know that

HTB Equity loans mean you borrow less, at a lower rate (from the banks, at least).

The winners in Equity Loans are the Government (through Capital Gains), and the developers (through having people buy their houses for artificially inflated prices).

Other schemes are different. Mortgage Guarantee helps the banks as it effectively makes 95% mortgages risk free. Shared Ownership helps Councils and Developers. Help to Buy ISAs help, er, nobody really, their a bit crap.

Last edited:

Caporegime

- Joined

- 18 Oct 2002

- Posts

- 37,804

- Location

- block 16, cell 12

"They struggled to afford a 3-bed semi" is a bit of a contradiction to the point you're trying to make, isn't it? I don't think many FTBs are really expecting to buy a 3-bed house, most in the SE are struggling to afford a 1-2 bed flat!

You only have to look around briefly online to show house prices versus earnings in relative terms to see it used to be 3-4x salaries, it's now 8-14x. The facts speak for themselves and the argument of 'expectations' is usually used by old baby-boomers that swiftly follow it up with "well I never had an iphone when I was 16yrs old".

The issue is that btl have capital and equity and are often able to bid cash. No seller can turn this down. I was beaten on 2 houses i wanted to buy in exactly this way.

As a first time buyer you won't have that much cash and the riskto tje seller is that the mortgage application falls through.

With LL's being able to command 2-3× the mortgage rate in rent the renters will really struggle to build the capital to put down a decent deposit. And when/if they do said capital holders can just gazump them anyway.

I get what you're saying and I agree with all your other points, but I'm just trying to say that HTB enables people to buy more expensive houses than they would have done without it. Therefore they are borrowing more from the bank because they are buying a more expensive house.HTB Equity loans mean you borrow less, at a lower rate (from the banks, at least).

eg. Before HTB a couple may have bought a £350k house. Now they can afford a £450k house.

I get what you're saying and I agree with all your other points, but I'm just trying to say that HTB enables people to buy more expensive houses than they would have done without it. Therefore they are borrowing more from the bank because they are buying a more expensive house.

eg. Before HTB a couple may have bought a £350k house. Now they can afford a £450k house.

The loan amount remains the same though. The difference is made up by the Equity Loan.

The loan amount calculations remain the same regardless. Like I said, I have recently been through this, as has my sister. Back when we were looking we could borrow up to £340k from the bank. With a 5% deposit that meant our budget was £388k. With an Equity Loan, our budget rose to £453k. The mortgage remained capped at a maximum of £340k in both cases, but the rate on the Equity Loan supported house was much less as it was 75% LTV rather than 95%.

The bank don't increase the amount they are willing to lend people because they have a larger deposit, they reduce the rate instead.

It would have been cheaper in terms of monthly payments for us to have bought a £453k house than it would have been to have bought a £388k one. The bank would have earned less from us had we got with Help to Buy Equity Loan.

The whole system is broken when me and my partner are paying £750 (per c/m) in rent down south and buying our first property (2 bed flat) up north for £55k to rent out and pay the mortgage that way.

We can't advance our careers up there as there is nob all opportunity (well a hell of a lot more competitive), and buying down here is obscene.

We can't advance our careers up there as there is nob all opportunity (well a hell of a lot more competitive), and buying down here is obscene.

Many of the sentiments in this thread echo my own ; The housing situation in this country is dire, and has disadvantaged an entire generation.

I've followed the housing market closely since 2010. Seeing the interventions and interference put in place by parliament has made me realise how disturbingly corrupt our government and financial system actually is.

The government relies on house price inflation to skew economic indicators in a favourable manner - it increases money supply, and ostensibly the wealth of a significant proportion of the voting demographic (mainly older people). It also positively impacts GDP; House prices and rents are both included in GDP. Even imputed rents for home owners (what a home owner would be paying in rent to live in their house) are included.

Help to Buy is a twisted piece of marketing genius. Masqueraded as a scheme to help first time buyers, when in reality the purpose of the scheme has been to increase the profitability of banks, house builders and benefit existing home owners through rising house prices.

There is some confusion on this thread over the help to buy scheme and how it works. There are several different versions of the scheme in operation, which I'll detail below;

Help to Buy:Equity Loan

Facilitated the purchase of new build properties with only a 5% deposit. The buyer contributes a 5% deposit, while the government provides a 20% equity loan, interest free for 5 years. The buyer would only have to secure a mortgage for 75% of the value of the property.

Because it specifically targeted new properties, it did result in the number of homes being built increasing slightly. The scheme's largest impact was on the profits and share prices of house building companies, which increased massively following the introduction of this scheme.

Help to Buy Mortgages

Introduced in 2013 in order to facilitate the reintroduction of 95% loan to value mortgages, for both new and old properties.

Following to the financial crisis, lenders were reluctant to lend more than 90% of property's value. Rather than allowing house prices to drop to a level at which a 10% deposit would be affordable, the government intervened.

The state will guarantee 20% of the mortgage value on specific 95% loan to value mortgages. Essentially, the state will hold the tab for the first 20% of losses, should the mortgage holder(s) default. This socialises the risk, while any profit will still go the bank.

This was widely criticised and by far had the greatest impact on house prices, which up until it's introduction, were stagnating.

Help to Buy ISA

Introduced in 2015, aspiring home owners can deposit an initial £1000, followed by a maximum of £200 per month. The government will contribute 25% of what you save to the purchase of a house. The maximum you can save under this scheme is £12,000.

Rather cynically, assuming you save the maximum £200 per month, this scheme would mature late 2019/ early 2020, just in time to boost house prices in time for the election.

Help to Buy is just the tip of the ice berg in terms of what the government have done to maintain and inflate house prices further.

In order to move forward, we need increased housing supply, not increased credit or financialisation.

Sadly a solution to housing affordability will not be forthcoming. The government are completely in control....

I've followed the housing market closely since 2010. Seeing the interventions and interference put in place by parliament has made me realise how disturbingly corrupt our government and financial system actually is.

The government relies on house price inflation to skew economic indicators in a favourable manner - it increases money supply, and ostensibly the wealth of a significant proportion of the voting demographic (mainly older people). It also positively impacts GDP; House prices and rents are both included in GDP. Even imputed rents for home owners (what a home owner would be paying in rent to live in their house) are included.

Help to Buy is a twisted piece of marketing genius. Masqueraded as a scheme to help first time buyers, when in reality the purpose of the scheme has been to increase the profitability of banks, house builders and benefit existing home owners through rising house prices.

There is some confusion on this thread over the help to buy scheme and how it works. There are several different versions of the scheme in operation, which I'll detail below;

Help to Buy:Equity Loan

Facilitated the purchase of new build properties with only a 5% deposit. The buyer contributes a 5% deposit, while the government provides a 20% equity loan, interest free for 5 years. The buyer would only have to secure a mortgage for 75% of the value of the property.

Because it specifically targeted new properties, it did result in the number of homes being built increasing slightly. The scheme's largest impact was on the profits and share prices of house building companies, which increased massively following the introduction of this scheme.

Help to Buy Mortgages

Introduced in 2013 in order to facilitate the reintroduction of 95% loan to value mortgages, for both new and old properties.

Following to the financial crisis, lenders were reluctant to lend more than 90% of property's value. Rather than allowing house prices to drop to a level at which a 10% deposit would be affordable, the government intervened.

The state will guarantee 20% of the mortgage value on specific 95% loan to value mortgages. Essentially, the state will hold the tab for the first 20% of losses, should the mortgage holder(s) default. This socialises the risk, while any profit will still go the bank.

This was widely criticised and by far had the greatest impact on house prices, which up until it's introduction, were stagnating.

Help to Buy ISA

Introduced in 2015, aspiring home owners can deposit an initial £1000, followed by a maximum of £200 per month. The government will contribute 25% of what you save to the purchase of a house. The maximum you can save under this scheme is £12,000.

Rather cynically, assuming you save the maximum £200 per month, this scheme would mature late 2019/ early 2020, just in time to boost house prices in time for the election.

Help to Buy is just the tip of the ice berg in terms of what the government have done to maintain and inflate house prices further.

In order to move forward, we need increased housing supply, not increased credit or financialisation.

Sadly a solution to housing affordability will not be forthcoming. The government are completely in control....

Last edited:

Please correct me if I'm wrong here but using your 100k example and my house is worth that. If tomorrow it was decided my house was worth 50k I stil have a mortgage for say 80k but a house that isn't worth that. I would never be able to afford to sell and essentially be stuck in a property forever. Is that not correct?

yes,. Welcome to the world of thousands who lost everything and became bankrupt when their mortgage was more than their house value.

It was a quick fix aimed at getting economic growth in time for the general election - give people free money and we shouldn't be surprised that results in economic growth. The problems will come in 5 years time when people start having to pay interest on this money - it's quite cheap at first but IIRC it goes up at the rate of inflation + 1% every year afterwards. If we don't get significant wage inflation in that time period then there will be issues. The great trick of course is that if the government borrows money then lends it out to other entities, it doesn't count towards our budget deficit.

The alternative would have been to invest in Britain's creaking infrastructure - it would have had greater results over the course of the long term, but of course the government wanted to push the austerity narrative.

Its fees not ibterest on the help to buy. And most people will remortgage and pay off it in one or chunks

Good summary HaX.

Shared Ownership also falls under the Help to Buy scheme. Where you own a percentage of a house with a deposit and a mortgage, and then a housing agency owns the rest and you pay rent on that part to the housing agency. It's basically privatised Council Housing and falls under the category of Affordable Housing. From experience, its crap. It is quite literally a scheme to get people into houses they can't afford and is really hard to get out of. The rules on the proportion of new builds that must be Affordable Housing is also reducing the supply of new houses to the 'normal' market.

Shared Ownership also falls under the Help to Buy scheme. Where you own a percentage of a house with a deposit and a mortgage, and then a housing agency owns the rest and you pay rent on that part to the housing agency. It's basically privatised Council Housing and falls under the category of Affordable Housing. From experience, its crap. It is quite literally a scheme to get people into houses they can't afford and is really hard to get out of. The rules on the proportion of new builds that must be Affordable Housing is also reducing the supply of new houses to the 'normal' market.

I rent my house in the UK out while I am in California, the rent exceeds my mortgage. I am hoping to save enough money while out here to have enough to get another house for me and my family to live in when we return and carry on renting out my old house.

I think instead of fighting against change people need to work with the system.

As a culture British people are way too hung up on owning their property and leaving the nest.

http://qz.com/167887/germany-has-one-of-the-worlds-lowest-homeownership-rates/

One of the reasons the financial industry gets attention now is the same reason that old industry did decades ago. It is the key industry for our country and the only reason we can even consider leaving the EU.

I think instead of fighting against change people need to work with the system.

As a culture British people are way too hung up on owning their property and leaving the nest.

http://qz.com/167887/germany-has-one-of-the-worlds-lowest-homeownership-rates/

One of the reasons the financial industry gets attention now is the same reason that old industry did decades ago. It is the key industry for our country and the only reason we can even consider leaving the EU.

Are you suggestion people should stay at home, or are you suggesting people should rent rather than buy?

The former is not the culture we have in the UK and wouldn't work for a lot of people. The latter is hindered by the UK rental market being unstable, insecure and expensive. I've lived in 3 rentals over 3 years due to get rich quick landlords or landlords on the cusp of affordability that then had to sell. And the house im currently buying with a 90% LTV is bigger, in a nicer area, and will cost us less a month than our current rental.

With house prices rising as they are owning property is also far better than savings. There's a reason were so hung up on owning property, its because its the sensible thing to do.

The former is not the culture we have in the UK and wouldn't work for a lot of people. The latter is hindered by the UK rental market being unstable, insecure and expensive. I've lived in 3 rentals over 3 years due to get rich quick landlords or landlords on the cusp of affordability that then had to sell. And the house im currently buying with a 90% LTV is bigger, in a nicer area, and will cost us less a month than our current rental.

With house prices rising as they are owning property is also far better than savings. There's a reason were so hung up on owning property, its because its the sensible thing to do.

I'm slightly lucky I suppose being in a council flat although it's getting crowded with the missus and 2 kids. For a 3 bed house in my town you're looking at £750 a month but the plan is to hold on to see if the council ever offer us something bigger, then perhaps buy it in time.

Now that I've finished uni we are only just in a position to seriously start saving and have some sort of target but it will be slow going and if prices just keep going up then its running after goalposts, renting privately would set us back even further.

I consider myself to be a in a good position, its particularly bad for minimum wage people on their own who will have to sink most of their months wages (at least a grand a month cheapest rent and conservative food) to live in a pokey flat.

Looking around on Rightmove the kind of houses I'd be interested in have doubled in price over the last 15 years

Now that I've finished uni we are only just in a position to seriously start saving and have some sort of target but it will be slow going and if prices just keep going up then its running after goalposts, renting privately would set us back even further.

I consider myself to be a in a good position, its particularly bad for minimum wage people on their own who will have to sink most of their months wages (at least a grand a month cheapest rent and conservative food) to live in a pokey flat.

Looking around on Rightmove the kind of houses I'd be interested in have doubled in price over the last 15 years

Its fees not ibterest on the help to buy. And most people will remortgage and pay off it in one or chunks

You can always tell when it's the evening. Tefal gradually starts morphing into Glaucus as the alcohol starts flowing...

Supply and demand is not to blame for the crazy prices:

availability of credit, particularly BTL and HTB are big factors in my opinion.

I do love an unlabeled axis so from 1997 till now the nunber of the uk population has increased from 100 to 110 and also that the whole time there has been more houses than people in the uk?

You can always tell when it's the evening. Tefal gradually starts morphing into Glaucus as the alcohol starts flowing...

I may have a drinking lroblem