Thanks for this. I didn't know this was an option.I transfer as much as I can from my workplace pension once a year to my Vanguard SIPP where it’s invested into the same index funds as my S&S ISA and Lifetime ISA. Some workplace pensions aren’t too bad on fees but some are awful so ymmv.

My current provider is The People's Pension. As others have mentioned, their fees are quite high and the fund options are limited. It looks as though they don't allow transfers out either, although I've emailed them to confirm this.

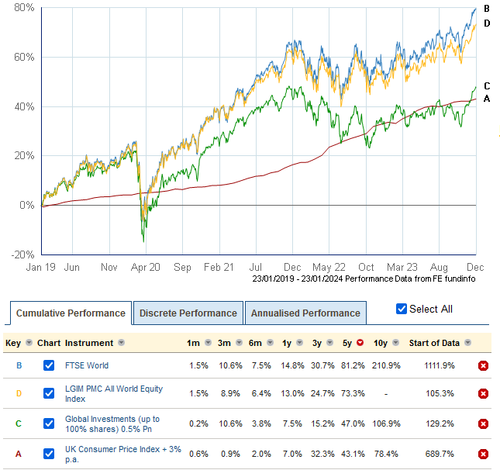

I've merged all of my older jobs into my last employers one (Legal and General), but I didn't consider transferring out of that into my own SIPP. Fees aren't too bad with L&G (0.35% annual management charge +0.13% for the fund), but there are cheaper options around. This has definitely prompted me to look around.

I'm 37 with a pretty measly pot. I've always contributed, but was low paid up until the last 5 years or so, and none of my employers have ever paid above the bear minimum.

My happy to go very high risk as retirement is a fair way off.

I also save into a S+S Isa and have built up a decent chunk in that. This is primarily a buffer for emergencies, but if I don't dip into it, will hopefully allow me to retire earlier by living live off it for a few years before having to break into my pension.