Soldato

- Joined

- 27 Mar 2004

- Posts

- 4,599

- Location

- Telford

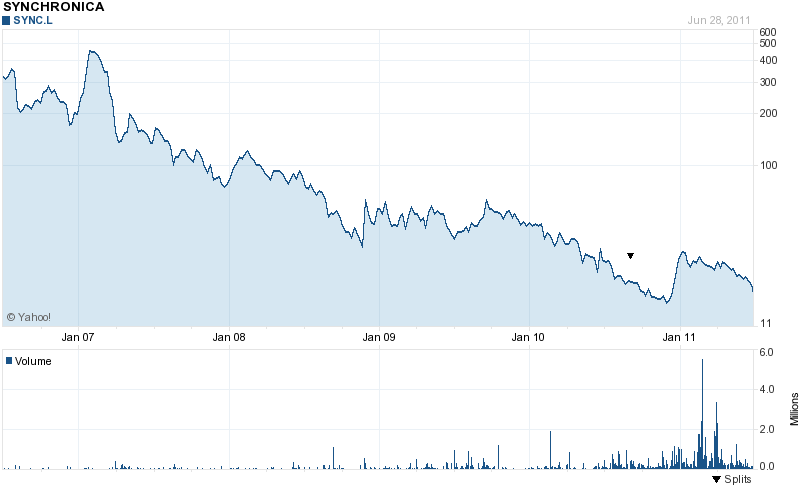

cnr @ 5 now, do i buy or wait? probably wait for a bit

cnr @ 5 now, do i buy or wait? probably wait for a bit

Its only gone up half a penny !

RNS Number : 1253J

Rockhopper Exploration plc

27 June 2011

Embargoed: 0700hrs, 27 June 2011

Rockhopper Exploration plc

("Rockhopper" or the "Company")

14/10-5 Appraisal well update - flow test result

Rockhopper Exploration, the North Falkland Basin oil and gas exploration company, is pleased to provide the following update on the flow test carried out at well 14/10-5.

· Well flowed at commercially viable rates

· Well flowed at stabilised rates of 5508 stb/d

· Well achieved a maximum stabilised flow rate of 9036 stb/d

A total section of 86m, incorporating 79m of reservoir, was perforated between 2379m and 2465m (md) over the Sea Lion Main Fan Complex. No lower fan sands were perforated on this flow test.

The well flowed for a main 48 hour flow period at a stabilised rate of 5508 stb/d and 940 mscf/d of gas with a flowing well head pressure (WHP) of 783 psi on a 48/64 inch choke. The gas oil ratio (GOR) was 170 scf/stb over the 48 hour period. The well was flowed through a separator under artificial lift by means of a downhole electric submersible pump (ESP). The flowing wellhead temperature was 62 degrees C. This temperature is significantly higher than that achieved during the test of well 14/10-2 and demonstrates the highly effective nature of the Vacuum Insulated Tubing (VIT) used during the test at 14/10-5. It was not necessary to use any wax inhibitors or pour point suppressants and no water or H2S were produced during the test.

The well was flowed for a second main flow during which the final maximum flow rate of 9036 stb/d was achieved with a flowing WHP of 625 psi on a fixed 1 inch choke over a 2 hour period before shutting the well in for a final build up and injectivity tests. The GOR during the maximum rate flow period was 153 scf/stb.

During the test down hole pressures were recorded and both surface and downhole crude oil samples were collected and will now be analysed by the Company.

Downhole mini DSTs (Drill Stem Test) were also performed on two of the three sands making up the 14m of net pay encountered in the well, which form part of the lower fan. These 2 sands had net pay of 8m and 4.5m. Interpretation of the results of the mini DST indicate that these 2 sands could have contributed an additional 800 stb/d flow rate using the same flow test techniques (artificial lift by ESP and thermal insulation by VIT) as used during the main DST performed on the upper fan in well 14/10-5.

The Board views the flow rates achieved as being commercially viable. Further appraisal drilling is being progressed over the coming months to continue to define the extent of the Sea Lion resource.

The Ocean Guardian drilling unit will now drill well 14/10-6, which will be the third appraisal well within the Sea Lion discovery area. 14/10-6 is located some 4.5km to the west of well 14/10-5 and is located within the Company's currently mapped mid-case area.

A further RNS will be issued after the well has spudded.

Sam Moody, Chief Executive of Rockhopper, commented:

"This very positive well test result is another key milestone in establishing Sea Lion commerciality. We will now review the wealth of data gathered during the testing process and continue our preparations for the next appraisal well on the field."

Enquiries:

Rockhopper Exploration plc

Sam Moody - Chief Executive

Tel. +44 (0)20 7920 2340 (via M: Communications)

M: Communications

Patrick d'Ancona or Ben Simons

Tel. +44 (0)20 7920 2340

Canaccord Genuity Limited

Charles Berkeley / Henry Fitzgerald-O'Connor

Tel. +44 (0) 20 7050 6500

Notes to Editors

Rockhopper was established in February 2004 with a strategy to invest in and carry out an offshore oil exploration programme to the north of the Falkland Islands. The Company floated on AIM in August 2005 and holds a 100 per cent. interest in four offshore production licences: PL023, PL024, PL032 and PL033 which cover approximately 3,800 sq. km. Rockhopper has also farmed in (7.5% working interest) to licences PL003 and PL004, which are operated by Desire Petroleum. These licences have been granted by the Falkland Islands government.

An extensive work programme has been carried out over a number of years on the licences operated by Rockhopper. This has included 2D and 3D Seismic and Controlled Source Electromagnetic Mapping (CSEM).

In February 2010, the Ocean Guardian drilling rig arrived in Falkland waters to carry out a multi-well drilling campaign. Rockhopper drilled an exploration well on its Sea Lion prospect during April and May 2010, the result of which was the first oil discovery and Contingent Oil Resource in the North Falkland Basin. The Sea Lion discovery was successfully tested during September 2010, and again in June 2011, and was the first oil to flow to surface in Falkland Islands waters. Rockhopper has contracted seismic vessels MV Polarcus Asima and Nadia to carry out a 3D seismic survey, beginning December 2010, over areas of licences PL024, PL032 and PL033 which were not previously defined by 3D, as well as adjacent areas.

Rockhopper Exploration plc

I just moved 1/3 of my holdings into cash, figure the next few months are going to be rocky!

Anyone in Cable & Wireless...?

INTERIM MANAGEMENT STATEMENT

Cable & Wireless Worldwide plc today confirms that its financial performance is in line with management expectations for the first 10 weeks of the 2011/12 year.

However, sales orders over this period, which contribute to margin growth later in the year, have been slower than expected. This recent trend combined with a lower than projected sales pipeline across our business indicates that our gross margin outturn is now expected to be somewhat below current market expectations.

This, coupled with an intention to accelerate the investments necessary to deliver growth in the hosting and cloud arena, is expected to lead to EBITDA outcome for 2011/12 some 5 to 10 percent below current market expectations with a commensurate impact on trading cash flow.

As a consequence of the reduced cash flow forecast, the Board has again reviewed the likely timetable to achieve dividend cover and has accepted that it is appropriate to reduce the intended dividend distribution for 2011/12 by half to 2.25 pence per share.

For the avoidance of any confusion, the final dividend of 3.00 pence per share relating to 2010/11 will be paid, as previously announced, on 11 August 2011 (subject to shareholder approval at the Annual General Meeting on 21 July 2011).

Directorate changes

In light of this, the Board of Cable&Wireless Worldwide has accepted the resignation of Jim Marsh and announces that John Pluthero, current Chairman of the Company, is to step into the role of Chief Executive. Senior Independent Director John Barton becomes Chairman of the Company and Penny Hughes is the new Senior Independent Director.

These changes are effective immediately.

John Pluthero comments: "Clearly it has been a very difficult 12 months and it is now important that we take the necessary steps to ensure the future growth of our business. I'll be looking to take a more radical approach to building on our hosting, cloud and data services business whilst becoming more competitive and efficient in the mature product areas. It has been easy to lose sight of what this business could be; it is my intention to reassert and realise that future."

John Barton says: "John Pluthero was the architect behind the successful turnaround of Cable&Wireless prior to demerger and knows the business and sector well. The Board has given John a full mandate to accelerate growth and maximise profitability."

The Company will release its interim results for the 2011/12 year in November 2011.

This weekly Briefing Note aims to pick out some of the key financial and economic issues touched on in the press over recent

days, and from time to time includes the views of some of our independent fund managers.

Chinese to the Rescue

Sovereign debt markets continued to take centre stage last week as policymakers went into overdrive to ensure a solution to the

Greek debt crisis. Investors watched with bated breath at the start of the week to see if the Greek government survived a crucial

vote of confidence which would then enable it to forge an agreement with the EU and IMF for a second bailout – conditional

though on a five-year austerity plan. The politicians had little choice, despite the rhetoric, but to say aye and Greece’s prime

minister survived the day, which meant financial markets could relax – a little. Analysts warned that there was yet another hurdle

insofar as the austerity measures still have to be passed by parliament this week before the next tranche of bailout funds could be

paid. Not that the outcome is guaranteed and some investors decided that the allure of safe havens such as German and US

government bonds, along with the Swiss franc was a better short-term alternative to the euro and Greek bonds. As an indication

of nervousness, five-year Greek credit default swap spreads – a gauge of the cost of insuring against a sovereign debt

default – climbed above 20% as the country’s crisis worsened.

The scale of the problem has been debated by the markets for a very long time so a stark warning from the chief executive of

Pimco, the world’s largest institutional bond investor, that debt default is the only solution for Greece, was met with equanimity.

But it seems that not everyone has lost confidence in the eurozone and specifically the raft of debt issued by its club-Med

economies. At the weekend the Chinese premier Wen Jiabao threw a lifeline to the eurozone, pledging to buy billions of euros of

European debt. “China is a long-term investor in Europe’s sovereign debt market. In recent years we have increased by quite a

big margin our holdings of government bonds. We will consistently continue to support Europe and the euro,” he said. His

comments came during his visit to Europe when he signed a number of deals with member countries, including Britain. Jim

O’Neill, chairman of Goldman Sachs Asset Management said the eurozone should look east for a solution to their continuing

debt problems. “Perhaps Europe’s leaders should try to put some of their differences aside and offer Asia’s yield-hungry

investors an even bigger kicker to help solve the crisis,” he commented.

Growth Stumbles

Away from Greece there were other issues for investors to mull over – not least of which were signs of slower growth in the

world’s largest powerhouses: America and China. HSBC’s flash Purchasing Managers’ Index, which tries to forecast the likely

position of both the full index and the official Chinese version, showed expansion in China’s manufacturing sector grinding to a

near standstill in June. It seems that this was a result of falling global demand and Beijing intensifying its efforts to suppress a

potentially destabilising credit boom. Whilst there is no concern about whether China continues to grow, the question is whether

the slowdown will cause a ‘soft’ or ‘hard’ landing. Analysts at HSBC dismissed fears of the latter scenario because year-on-year

industrial production in China is growing at a double-digit percentage pace. The country’s slowdown may be impacting

elsewhere too – growth in the eurozone has also slowed in recent weeks, according to the ECB, and without relatively strong

performances by Germany and France, the region’s private sector would have shrunk.

But it was the more subdued message from the US that investors found most disconcerting. The Financial Times noted that last

week’s meeting of the US Federal Reserve’s FMOC left a pretty downbeat impression of weaker than expected growth for the

country, with the market’s worries compounded by disappointing weekly labour data. Not that it was all bad news – growth for

first-quarter GDP was revised up slightly to 1.9%, albeit still down from the robust 3.1% in the last quarter of 2010. Whilst

businesses continue to restock, slower export growth and cuts in government spending offset this. Higher inflation is also

beginning to make itself felt, as shopping and fuel bills rise, causing consumers to cut back; although overall spending still grew

by 2.2% during the period.

Oil on Troubled Waters

American economist Irwin Stelzer, writing in The Sunday Times, put the current situation neatly into context by contrasting the

Fed’s policies with those of President Obama. Fed chairman Ben Bernanke has obligingly printed and spent a further $600bn,

buying the President’s IOUs (colloquially known as QE) in the expectation that the economy would grow at 3.5% and that low

interest rates would boost the troubled US housing markets. Neither has happened and the result has been costly: the budget

deficit is around 10% of GDP (almost in line with Greece) and the Fed’s own balance sheet has mushroomed to $3 trillion.

Unemployment is still over 9% and, as said, growth is only 1.9%. By its own admission the Fed is nonplussed, with Mr

Bernanke saying, “We don’t have a precise read on why this slower pace of growth is persisting” and consequently has

downgraded this year’s growth forecast to 2.9%. However, Mr Bernanke has stuck to his promise not to print

more dollars and has confirmed that the current QE programme will end this month.

Contrast this with Mr Obama’s own policies which are predicated on the idea that deficit spending will get the

economy moving again. So the peace dividend from troop reductions in Afghanistan will be spent on

infrastructure and green energy. He continues to resist calls by the Republicans to cut spending and not to raise

taxes. Stelzer opined that it was no surprise that with this level of partisan dispute, businesses and consumers

were nervous and unlikely to start spending in the way Mr Obama would like, which would boost growth and cut

unemployment. So what to do? Well, the markets found out late last week as news broke that, for only the third

time in its history, the International Energy Agency (which includes the UK, US, Japan et al) decided to release

some of its strategic oil reserves – 60m barrels over the next 30 days. The reaction was immediate – oil prices

plunged, with Brent crude falling by 8.5% as traders were caught off-guard.

The ostensible reason for one of the Agency’s most daring moves ever was that it was necessary to replace the

high quality oil being lost from Libya. But it became clear that the move was intended to tackle the damage being

done to world growth by the $100-plus per barrel cost of oil. The task had obviously required delicate diplomacy,

said The Financial Times, with Washington needing to be sure Saudi Arabia would not tighten supply to push

up prices. Western policymakers were no doubt pleased with the outcome, although there was speculation that

whilst bold, the move would only give temporary respite. Either way, the timing of the announcement has

coincided neatly with the start of America’s ‘driving season’ when most of the population take to their cars and

go on holiday. It could, thought The Sunday Telegraph, also be the start of President Obama’s re-election

campaign. Over in the financial markets the news caused little immediate reaction outside commodity prices,

with stock markets continuing their weekly meandering. By the close of business it was easy to see the

winners – most of Asia’s major indices advanced substantially over the week, led by China’s Shanghai Stock

Exchange Composite Index which was up almost 4%. In contrast, Europe followed Wall Street marginally lower

as investors ruminated over slower US growth and sovereign debt issues.

Confidence with Caution

Against the backdrop of choppy markets it’s useful to have an insight into the thoughts and actions of

professional investors who, on a daily basis, have to interpret the ebb and flow of both good and bad news alike

as part of their job. One of the City’s most respected fund managers, Adrian Frost of Artemis, explains his

strategy. “High level, my investment style is to concentrate on income so my strategy is not strongly based on the

global, macro issues although I do, of course, observe these and have to weigh up how economically sensitive a

stock might be. I’m looking for companies that are good quality, have good growth prospects and can increase

their dividends. The portfolio currently yields around 4.1% [net of basic rate tax] and with good cash flows, I

have been able to add the stocks I like – I’d rather buy on days when the market is down as it helps average-in

costs.

“The portfolio is centred around what the market calls a ‘risk-off’ approach – in other words, safer, lower-risk

companies who can grow their businesses even if the economic environment becomes less favourable. For

example, Deutsche Post has all the characteristics I like. It is a market leader in logistics, delivering globally with

particular emphasis on emerging markets. It is a market leader in e-retailing (Amazon) and at home has a core

income because of state requirements for utility bills and bank statements to be posted to customers. Currently it

is about half as profitable as its competitors but has recently invested heavily in its business and it is enjoying

parcel growth of 10% – every new parcel added is highly profitable. I also own capital goods company Melrose

which, like many of its competitors, is experiencing some slowdown. However the company has two main

businesses – manufacturing power generators which is a growth sector as businesses invest in gas, and Bridon

which is geared into energy via the development of oilfields in Brazil.

“The outlook for dividends is positive with a likely increase across the board of c5%–10% – ahead of inflation.

In fact, dividends have increased at around 8% per annum over the last decade, despite the recession. I think

there is a low probability that good quality companies will cut their dividends in the way they did during the

financial crisis. Then they were wrong-footed and some found themselves having to refinance corporate bonds at

very high levels. They have learnt their lesson and the type of company I deal with is determined not to get

caught out again, hence the high levels of corporate cash we currently see. This gives me a lot of confidence

going forward that I can expect dividends to be maintained or increased. Also there is increased merger and

acquisition activity – the portfolio could benefit on both counts as some of my holdings could be acquisitors

because they are cash rich and, conversely, become attractive to a larger business because they are cash

rich – one holding, Laird Group, is currently subject to a takeover bid. Geographically the portfolio is heavily

weighted toward the UK but the income element is very diverse, with much being derived internationally

including emerging markets, which itself accounts for c15% of earnings, so there are good growth prospects for

investors over the medium to long term.”

Anyone bullish on Apple ? ipad 3 for xmas

Anyone in Cable & Wireless...?