I guess Morrison tie up shows demand for their service product. Very good volume, up nearly a third at one point.

I dont think you should kick yourself if you made a profit, selling at the top is a bit of a myth for most of us. Mostly Ive learnt to buy and sell in parts not all at once if possible.

Also depends what you buy now instead of

OCDO. When I sold BB to buy SL, it looked like I screwed up because BB price kept going up. But they went to zero so imo taking profits is never regretful.

SL was a dirt cheap forced flotation, BB was overrated, over-anticipated

while that of Morrisons added almost 2%.

"The agreement will enable Morrisons to enter the online grocery market quickly with a profitable business model," Morrisons said in a statement.

I think Questor mentioned buying Morrisons. Its one idea to buy the partner in a deal, sometimes can be clever and/or safer.

Certainly MRW pay 4% yield, I like that at 10 PE. Just went exdiv

BP has some negative news right now, but they appear to be a solid hold anyway

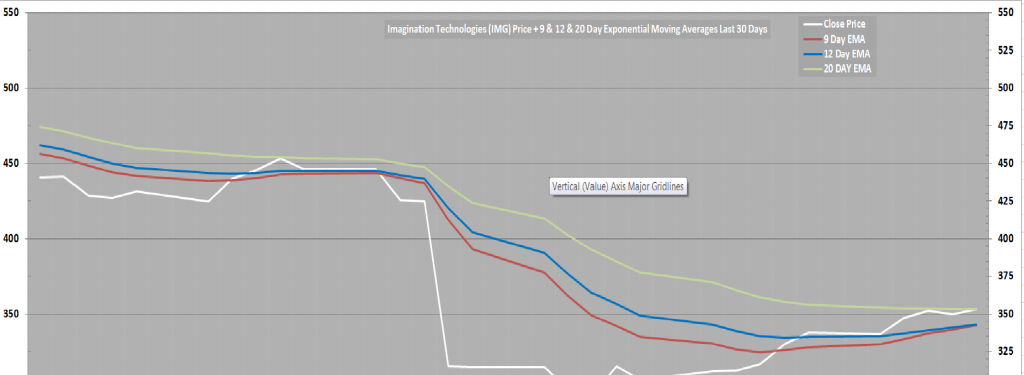

PCT (tech) I was just pointing out to a long term holder has a rising wedge which can be very negative.

Every peak price is not really gaining anything. Eventually a lot of investors sell out from having seen no real gains, is the idea

My idea on GKP is now is nothing special. I hope it spins up wildly like OCDO because I own a bit but Im not chasing it or adding any.

Volume is good but not brilliant, I dont expect it to exceed 200. If we're speculating on buying the bottom, I dont think its done it yet.

Probably like BP it has to clear a lot of the negatives before it can power ahead, barring the worst its fairly obvious it will be a lot higher one day

It makes no sense for HMG to flood the market and push the price below their initial purchase price.

Instead of a div, Lloyds could buy shares back from government. I think thats allowed and they are able.

Without a white knight, it'll take a while to buy them all back.

The other idea is gov gives away/IPO on RBS and Lloyds before election

")